SOX Compliance Without the Spreadsheet: What Auditors Actually Want to See in IAM 2026

SOX §404 requires access controls that produce evidence, not policy documents that describe them. The 2026 enterprise reference on the four IAM access-control domains SOX auditors probe, the five reports they'll ask for, and the architecture that generates them on-demand rather than in the quarter-end scramble.

SOX §404 requires access controls that produce evidence, not policy documents that describe them. The 2026 enterprise reference on the four IAM access-control domains SOX auditors probe, the five reports they'll ask for, and the architecture that generates them on-demand rather than in the quarter-end scramble.

- SOX §404 access controls concentrate in four IAM domains: privileged access (who has admin rights to financial systems), financial-system access (who can create/approve/reconcile transactions), segregation of duty (which entitlement combinations create fraud paths), and lifecycle deprovisioning (departed employees who retain access are the most common SOX finding).

- Five reports come up in nearly every SOX audit cycle: current entitlement snapshot per financial system, quarterly entitlement changes with approver evidence, SoD violation report with disposition, dormant account report with removal disposition, and privileged access recertification results.

- Most SOX-relevant IAM incidents come from the same source: entitlement state that diverged from documented policy between certifications, without anyone noticing until the audit surfaced it. The IGA workflow's job is to prevent divergence; the audit-trail architecture's job is to prove it.

- The 2026 architectural test isn't whether the reports exist — it's whether the reports can be generated on-demand rather than assembled in a two-week quarter-end scramble. Continuous audit readiness is the goal; the audit cycle becomes a snapshot, not a scramble.

- Avatier maintains SOC 2 Type II with zero exceptions, ISO/IEC 27001:2022, NIST 800-53 Rev. 5 aligned posture, and is a CISA Secure-by-Design Pledge signatory — all published at trust.avatier.com. Customer SOX programs benefit from an IGA platform whose own vendor posture is auditable.

Sarbanes-Oxley §404 is one of the most cited but least understood regulatory drivers of enterprise IAM. Most organizations know they have SOX obligations. Most audit teams know IAM is load-bearing for those obligations. Yet SOX audits routinely surface access-control findings that everyone in the organization would have said were "already handled." The gap is almost never a missing policy. The gap is that the actual entitlement state diverged from the documented policy between certification cycles, and nobody detected the divergence until the audit surfaced it.

This piece is the 2026 enterprise reference on SOX §404 access controls in IAM — the four domains auditors probe, the five reports they'll ask for, and the architecture that generates continuous audit readiness rather than the two-week quarter-end scramble. The companion pieces cover adjacent territory: the Access Review Auditor Wants piece covers the horizontal review discipline this composes with; the PCI-DSS v4.0.1 piece covers the payment-card compliance regime; the HIPAA §164.312 piece covers healthcare-specific controls. Under the hood, the same IGA + ISPM + AI-augmented certification stack supports all four compliance regimes — the audit surface differs, the architecture doesn't.

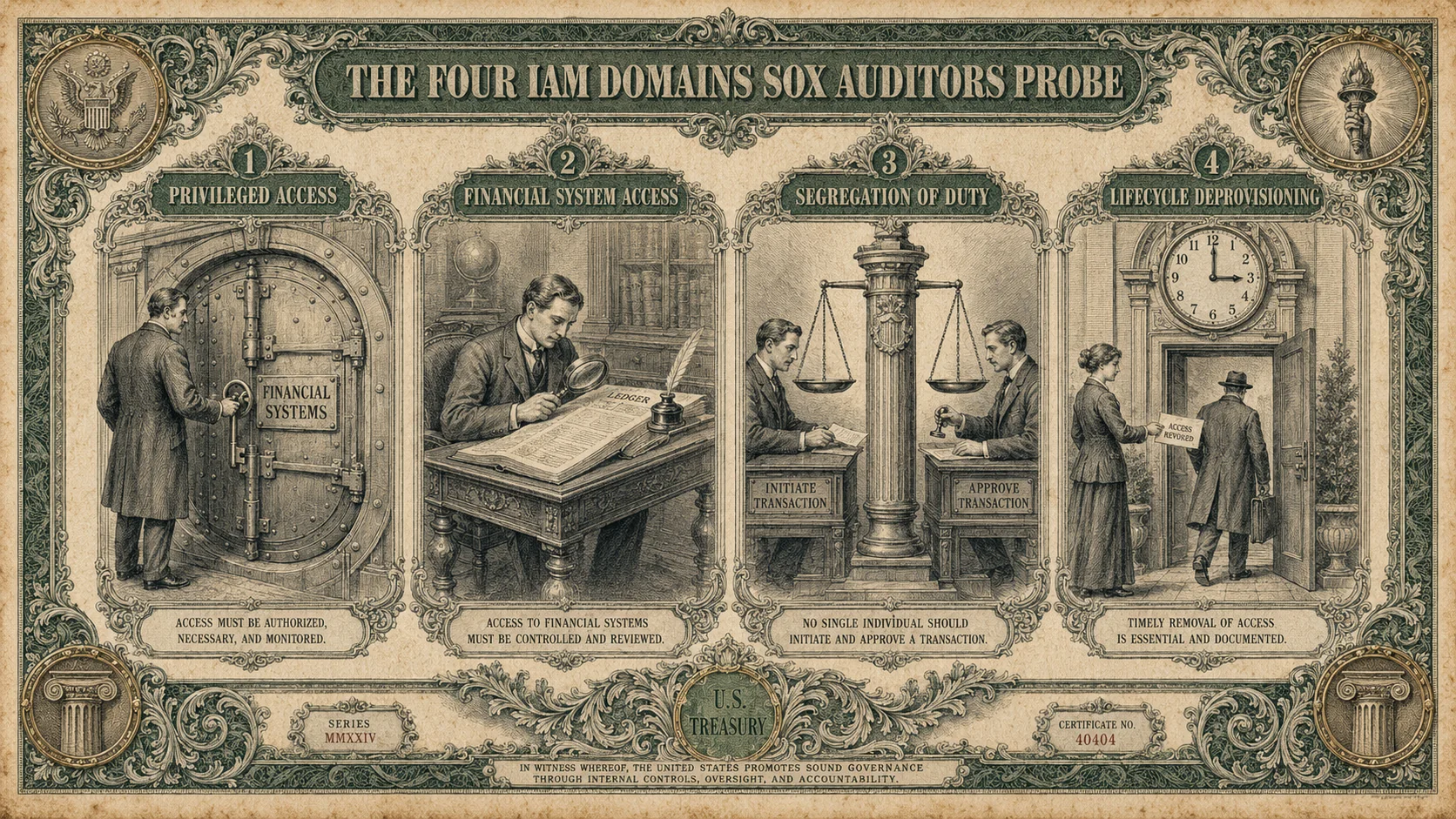

Four IAM domains, one auditor's magnifying glass. SOX §404's IAM surface concentrates here; the audit's evidence questions come from these four places.

Four IAM domains, one auditor's magnifying glass. SOX §404's IAM surface concentrates here; the audit's evidence questions come from these four places.

What SOX §404 actually asks of IAM

Section 404 of the Sarbanes-Oxley Act of 2002 requires public companies (and certain private companies acquired by public companies, or preparing to go public) to establish and maintain adequate internal control over financial reporting (ICFR). Management assesses those controls annually; external auditors attest to the assessment. The word "adequate" is where all the operational discipline lives — SOX doesn't specify particular IAM controls, but it does expect the organization to demonstrate that access to financial systems is appropriately governed.

"Appropriately governed" translates operationally into four testable claims the organization makes and the auditor probes:

Claim 1: Access is granted per documented business justification. For every user with financial-system access, the organization can produce a documented reason the access was granted, an approval workflow record showing who approved it, and evidence that the access matches the user's current role.

Claim 2: Access is restricted per segregation-of-duty policy. The organization has defined SoD rules that identify entitlement combinations creating fraud paths (originate a payment + approve the same payment + reconcile it, all in one user); those rules were enforced at grant time; violations that exist have documented mitigating controls.

Claim 3: Access is reviewed periodically with auditable evidence. Certification campaigns ran on schedule during the audit period; reviewers actually engaged with the entitlements (not just clicked through); disposition records exist for every reviewed entitlement.

Claim 4: Access is removed when no longer needed. When users changed role or left the organization, their financial-system access was removed within a defensible window; timestamps prove the removal happened; there aren't departed employees with active access at the time of the audit.

Every SOX §404 IAM finding maps to one of the four claims failing verifiably. The finding isn't that the organization lacks a policy — it's that the policy and the reality diverged in a way the organization can't excuse.

The four IAM domains SOX auditors probe

The four SOX §404 claims concentrate audit attention on four IAM domains. Each has characteristic finding patterns; each has a characteristic architectural mitigation.

Domain 1: Privileged access to financial systems. Administrative privileges on the ERP (SAP, Oracle Cloud ERP, NetSuite, Workday Financials), general ledger, payment systems (treasury workstations, wire origination systems), and reconciliation platforms. Auditors ask: who has admin? Is the admin population justified by current role? How is the admin population certified? Is there just-in-time elevation for admin functions or standing admin access? Standing admin access to financial systems is a red flag in 2026 audits; just-in-time (JIT) elevation with recorded sessions is the mature pattern. The PAM piece covers this layer in depth.

Domain 2: Financial-system access beyond privileged. The broader population of users who can create, modify, approve, or reconcile financial transactions. Auditors ask: does the assignment match the role definition? Are role definitions current and documented? When a user changed role, did their financial-system access shift with the role change? The findings in this domain concentrate on mover events that stacked entitlements instead of substituting them — the HRIS-Driven Lifecycle piece covers the mover-workflow architecture that prevents this.

Domain 3: Segregation of duty. The SoD rule set defines which entitlement combinations create fraud paths. Auditors ask: what's your rule set? When was it last reviewed? What violations exist right now? What's the disposition for each? SoD findings come from three failure modes — the rule set is stale relative to current business processes, violations exist without documented mitigating controls, or violations exist that the organization didn't know about because SoD evaluation only runs at grant time and not against the accumulated entitlement state. The 2026 architectural pattern evaluates SoD both at grant time (catch new violations) and at recertification (catch accumulated violations from paths the grant-time evaluation missed).

Domain 4: Lifecycle deprovisioning. The most common source of SOX §404 findings. Departed employees who retain financial-system access is exactly the kind of finding auditors specifically look for because it's easy to prove and hard to explain. Auditors run a simple test: pull HR termination records for the audit period, cross-reference with current entitlement state, list any user whose termination date is in the past but whose entitlements are still active. The number of hits determines the severity of the finding. The 2026 mature pattern closes the leaver-to-deprovisioning gap to under 24 hours at the 99th percentile via HRIS-driven leaver automation — the HRIS-Driven Lifecycle piece covers this closure.

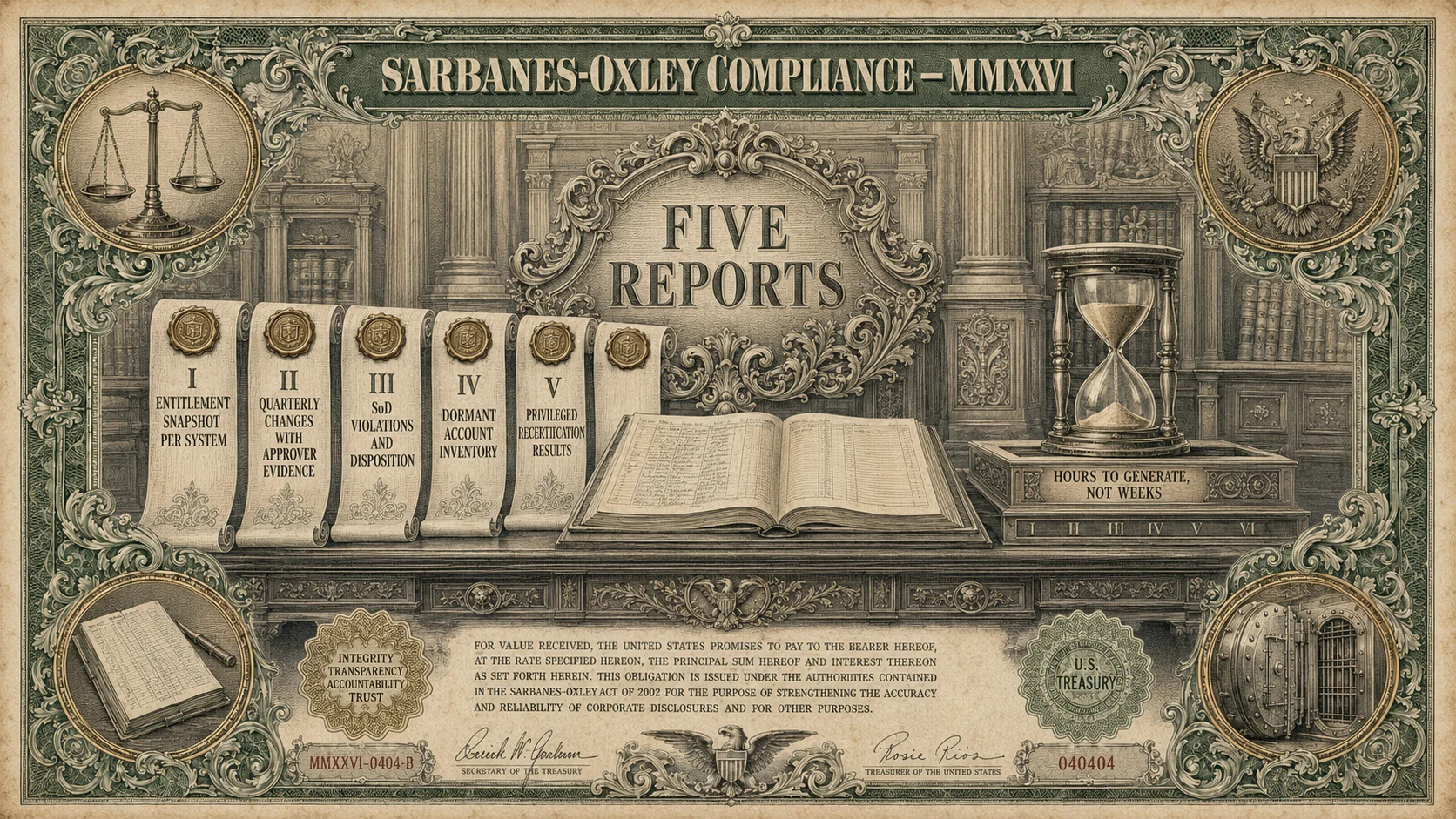

The five reports auditors ask for at every cycle

The audit interview is often theatrical; the audit evidence request is not. Five reports come up nearly every SOX audit cycle for organizations with mature IAM programs. The 2026 architectural test is whether they can be generated on-demand.

| Report | What auditor asks | 2026 target answer |

|---|---|---|

| Entitlement snapshot per financial system | "Show me who currently has access to [SAP / Oracle / etc.]" | Generated in minutes from the IGA platform |

| Quarterly entitlement changes with approver evidence | "Show me what changed since last quarter and who approved each change" | Generated from the IGA workflow audit log |

| SoD violation report with disposition | "Show me current SoD violations and how each is being managed" | Generated from the IGA rule engine |

| Dormant account report | "Show me accounts that haven't been used in 90+ days" | Generated from IdP + target-system telemetry |

| Privileged access recertification results | "Show me the last certification campaign for privileged accounts" | Generated from the certification campaign record |

The reports don't need to be generated live during the audit — auditors typically request them at the start of fieldwork and expect them within a defined window (often 5-10 business days). The 2026 mature architecture produces them in hours because the underlying data is already structured; the immature architecture produces them in weeks because the underlying data has to be reconstructed from scattered sources.

The gap between the two isn't the presence of an IGA platform. Every organization with a SOX obligation of any scale has an IGA platform. The gap is whether the IGA platform's audit-trail architecture actually produces the reports without human intervention, or whether the IGA platform is a workflow tool that leaves auditor-facing reporting as an exercise for the compliance team at quarter-end.

Where SOX audits break: the divergence patterns

Every SOX §404 IAM finding is fundamentally a policy-vs-reality divergence. Four divergence patterns recur.

Divergence 1: Termination-to-deprovisioning delay. HR records a termination on day zero; IAM removes financial-system access on day N. If N is 30 or 60 or "sometime," the audit finds it. The mitigation is HRIS-driven leaver automation with real-time (or near-real-time) event propagation — the HRIS-Driven Lifecycle piece covers the integration patterns that close the window.

Divergence 2: Mover stacking. User transitions from Accounts Payable to Treasury; AP entitlements were never removed; user now has AP entitlements + Treasury entitlements simultaneously, which produces a SoD violation. The mover-workflow architecture must diff the target entitlement set against the current entitlement set and apply both additions and removals — the HRIS-Driven Lifecycle piece covers the mover-specific logic.

Divergence 3: Shadow provisioning. Access grants that happened outside the IGA workflow — through direct system admin, ITSM tickets that bypassed IGA approval, Slack requests, manager Excel uploads. The IGA catalog reflects only what IGA granted; the target-system reality diverges. Auditors detect this by reconciling the IGA catalog against target-system extracts. The Shadow IT Provisioning piece covers the architectural pattern that captures shadow provisioning back into governance.

Divergence 4: Certification fatigue. Reviewers pattern-click through certification campaigns, approving entitlements they didn't examine. Auditors probe by asking reviewers about specific decisions — "why did you approve this user's access to system X?" — and find blank looks. The AI-augmented certification pattern (covered in the AI Access Certification piece) increases engagement discipline by pre-stratifying decisions and enforcing reviewer engagement on the highest-risk categories.

The four divergence patterns are operationally manageable when they're the design target. They're audit findings when they're not. The 2026 mature IGA architecture treats all four as design constraints from the start.

Five reports, five wax seals. The 2026 mature architecture generates them in hours from structured underlying data; the immature pattern reconstructs them in weeks at quarter-end.

Five reports, five wax seals. The 2026 mature architecture generates them in hours from structured underlying data; the immature pattern reconstructs them in weeks at quarter-end.

The 2026 reference architecture for SOX audit readiness

Composing the pieces produces continuous audit readiness — the audit cycle becomes a snapshot, not a scramble. The reference architecture has six layers.

Layer 1: HRIS-driven lifecycle. Joiner-mover-leaver events originate from the HRIS (SAP SuccessFactors, Workday, ADP, others) and propagate to IAM through SCIM push, delta synchronization, and full reconciliation — closing the divergence-1 (termination delay) and divergence-2 (mover stacking) gaps. The HRIS-Driven Lifecycle piece covers the integration patterns.

Layer 2: IGA workflow. Access requests, approvals, provisioning, and recertification all run through documented workflow with audit-trail records. The workflow catalog stays current with target-system reality via periodic reconciliation. The Best IGA Solutions piece covers platform-level evaluation.

Layer 3: SoD rule engine. Segregation-of-duty rules evaluate at grant time and at recertification, catching both new violations and accumulated violations. The rule set gets reviewed with business-process owners on a defined cadence to stay current with organizational reality.

Layer 4: Shadow provisioning capture. Target-system reconciliation surfaces entitlements that arrived through shadow paths; ticket-system integration routes access tickets through IGA approval; governed self-service makes the IGA path competitive on speed and UX so shadow paths lose their appeal. The Shadow IT Provisioning piece covers this layer.

Layer 5: AI-augmented certification. Certification campaigns pre-stratify entitlements for reviewer attention, enforce reviewer engagement on high-risk categories, and produce structured disposition records for audit. The AI Access Certification piece covers this layer.

Layer 6: ISPM posture audit. Between certification cycles, ISPM continuously evaluates posture and surfaces findings the campaign cycle would miss — drift, dormant entitlements, orphaned admin accounts. The ISPM piece covers the preventive posture-audit layer.

The six layers compose into an architecture where the five auditor reports are always ready to generate. The audit becomes an evidence request rather than an assembly project.

The Avatier compliance posture matters for customer SOX programs

SOX audit scrutiny increasingly extends to vendor supply chain. When customers use Avatier Identity Anywhere Lifecycle Management as their SOX-relevant IGA platform, the audit will probe Avatier's own compliance posture — is the vendor auditable, is its own control environment sound, does it publish evidence customers can attach to their vendor-management story.

The Avatier Trust Center publishes our compliance posture and audit evidence. The current posture:

- SOC 2 Type II with zero exceptions — the most-referenced audit for vendor management

- ISO/IEC 27001:2022 — the international standard for information security management systems

- PCI DSS v4.0.1 — the current normative for payment card data (also relevant when Avatier customers process cardholder data alongside financial data)

- CSA STAR Level 1 — cloud security posture attestation

- NIST 800-53 Rev. 5 aligned — the federal control framework, useful for public-sector customers and financial services organizations mapping to FFIEC / SR 11-7

- CISA Secure-by-Design Pledge signatory — the 2024 CISA framework Avatier committed to

The third-party security grade view (SecurityScorecard) is at trust.avatier.com/?itemName=security_grades. Customer SOX audit teams that ask for Avatier's compliance evidence can be pointed directly at the Trust Center rather than routed through procurement questionnaires.

The 2026 reference path

Treat SOX §404 IAM compliance as a design target, not a periodic audit response. Build the six-layer reference architecture — HRIS-driven lifecycle, IGA workflow, SoD rule engine, shadow provisioning capture, AI-augmented certification, ISPM posture audit — and the five auditor reports become byproducts of the architecture rather than assembly projects.

Focus the four divergence patterns as design constraints. Close the termination-to-deprovisioning window with HRIS-driven leaver automation. Prevent mover stacking through explicit diff-and-substitute logic in the mover workflow. Capture shadow provisioning through target-system reconciliation and ticket-system integration. Enforce reviewer engagement in certification through AI-augmented pre-stratification.

Point auditors at the Trust Center for Avatier's own compliance evidence. Customer SOX programs get a stronger vendor-management story when the IGA vendor's compliance posture is public, current, and auditable — the Avatier Trust Center is the answer.

SOX audits will keep happening annually. The audit cycle can be a scramble that consumes the compliance team for weeks, or it can be a snapshot that generates the reports in hours. The architectural discipline determines which. Choose the architecture deliberately — the audit cycles of 2027, 2028, and 2029 will reward the choice.

ABOUT THE AUTHOR

More from Compliance & Audit

SOX Compliance for Identity Teams 2026: What Auditors Actually Want to See

Sarbanes-Oxley Section 404 places IT general controls (ITGC) over financial systems squarely in the IAM team's lap — even though SOX itself doesn't mention identity once. The 2026 enterprise reference on the five SOX ITGC domains that depend on identity controls, the auditor expectations that shifted in the post-2025 audit cycle, and the architecture that produces clean SOX walkthroughs.

HIPAA Access Audits for Healthcare Identity Teams 2026

HIPAA Security Rule § 164.312 places identity controls at the center of every covered entity's access-audit risk. OCR enforcement actions have intensified through 2024-25, and the 2026 audit profile is substantively harder than the prior decade. The enterprise reference on the five Technical Safeguards that depend on identity controls, the post-2024 OCR enforcement pattern, and the architecture that produces defensible HIPAA access-audit posture for healthcare IT.

The Access Review Your Auditor Actually Wants 2026

Most enterprise access reviews are checkbox exercises — manager attests, audit log records, cycle closes. The auditor walks away with a binder of attestation evidence and the program reports clean. The 2026 auditor profile asks harder questions: did the reviewer actually engage, does the catalog match target-system reality, and what changed as a result. The enterprise reference on the three questions auditors actually ask now and the five review patterns that pass the test.