The Access Review Your Auditor Wants vs What You're Running 2026

Most enterprise access reviews are checkbox exercises that pass IAM policy but fail audit scrutiny. The 2026 enterprise reference on the three questions auditors ask that checkbox reviews can't answer, the risk-weighted review architecture that produces defensible evidence across SOX, PCI-DSS, HIPAA, and SOC 2 simultaneously, and the operational patterns that make the shift sustainable.

Most enterprise access reviews are checkbox exercises that pass IAM policy but fail audit scrutiny. The 2026 enterprise reference on the three questions auditors ask that checkbox reviews can't answer, the risk-weighted review architecture that produces defensible evidence across SOX, PCI-DSS, HIPAA, and SOC 2 simultaneously, and the operational patterns that make the shift sustainable.

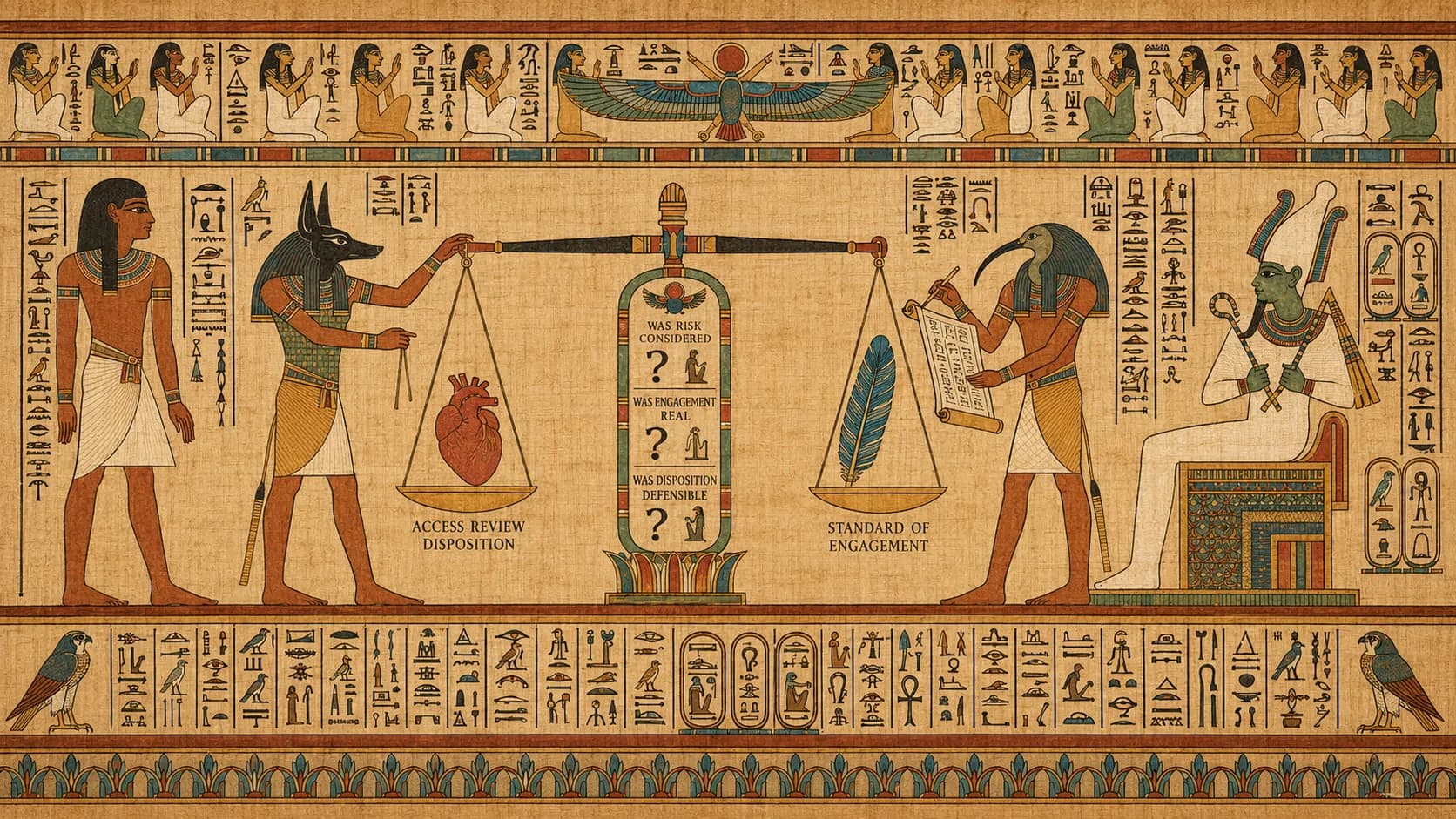

- Three questions auditors ask that checkbox reviews structurally cannot answer: (1) Was risk actually considered — did the review differentiate high-risk entitlements from routine ones? (2) Was reviewer engagement real — did the reviewer actually examine the entitlements, or pattern-click through them? (3) Was disposition defensible — for each entitlement reviewed, is there a specific reason for the disposition beyond 'approve to close the campaign'?

- A checkbox review completes the required cadence and produces a signed attestation, but the underlying evidence is uniform and unhelpful — every entitlement approved, no differentiation, no engagement trace, no disposition context. Auditors probe the evidence and find nothing they can use.

- The risk-weighted review architecture solves all three questions simultaneously: entitlements are pre-stratified by risk before the reviewer sees them, reviewer engagement is instrumented (time-on-decision, mouse-hover, periodic challenge questions), and disposition captures specific context beyond a binary approve/revoke.

- The same review architecture that produces SOX-defensible evidence also produces PCI-DSS v4.0.1-defensible, HIPAA §164.312-defensible, and SOC 2 CC6.x-defensible evidence — the compliance regimes differ in their finding surface but expect the same underlying review discipline.

- Avatier maintains SOC 2 Type II with zero exceptions, ISO/IEC 27001:2022, PCI DSS v4.0.1, and NIST 800-53 Rev. 5 aligned posture — published at the Avatier Trust Center. Customer audit programs benefit from an IGA vendor whose own review discipline produces auditable posture.

Enterprise access reviews are one of the most consistently under-performing compliance activities in modern IT. The compliance calendar mandates them (quarterly or semi-annual, depending on regime). The IGA platform runs them. The reviewers complete them. The attestation gets signed. The audit cycle passes. And then — quietly, in the actual audit interviews — auditors ask questions the review can't answer, and findings emerge that everyone thought were prevented by the review having happened.

The gap is structural. Most enterprise access reviews are checkbox exercises: uniform lists of entitlements, uniform disposition options, uniform time pressure, uniform evidence trail. They complete the required cadence and produce a signed attestation. But the evidence they produce is uniform and unhelpful. Auditors probe and find nothing they can use to validate that the review actually accomplished what compliance policy said it should.

This piece is the 2026 enterprise reference on the horizontal review discipline that ties together the compliance regimes covered in this series. The SOX Compliance piece covers §404 IAM controls. The PCI-DSS v4.0.1 piece covers cardholder data environment controls. The HIPAA §164.312 piece covers ePHI technical safeguards. This piece covers the review discipline that produces defensible evidence for all three (plus SOC 2, ISO 27001, and any other regime that audits access) simultaneously. The three auditor questions and the risk-weighted review architecture that answers them are the horizontal that unifies the compliance stack.

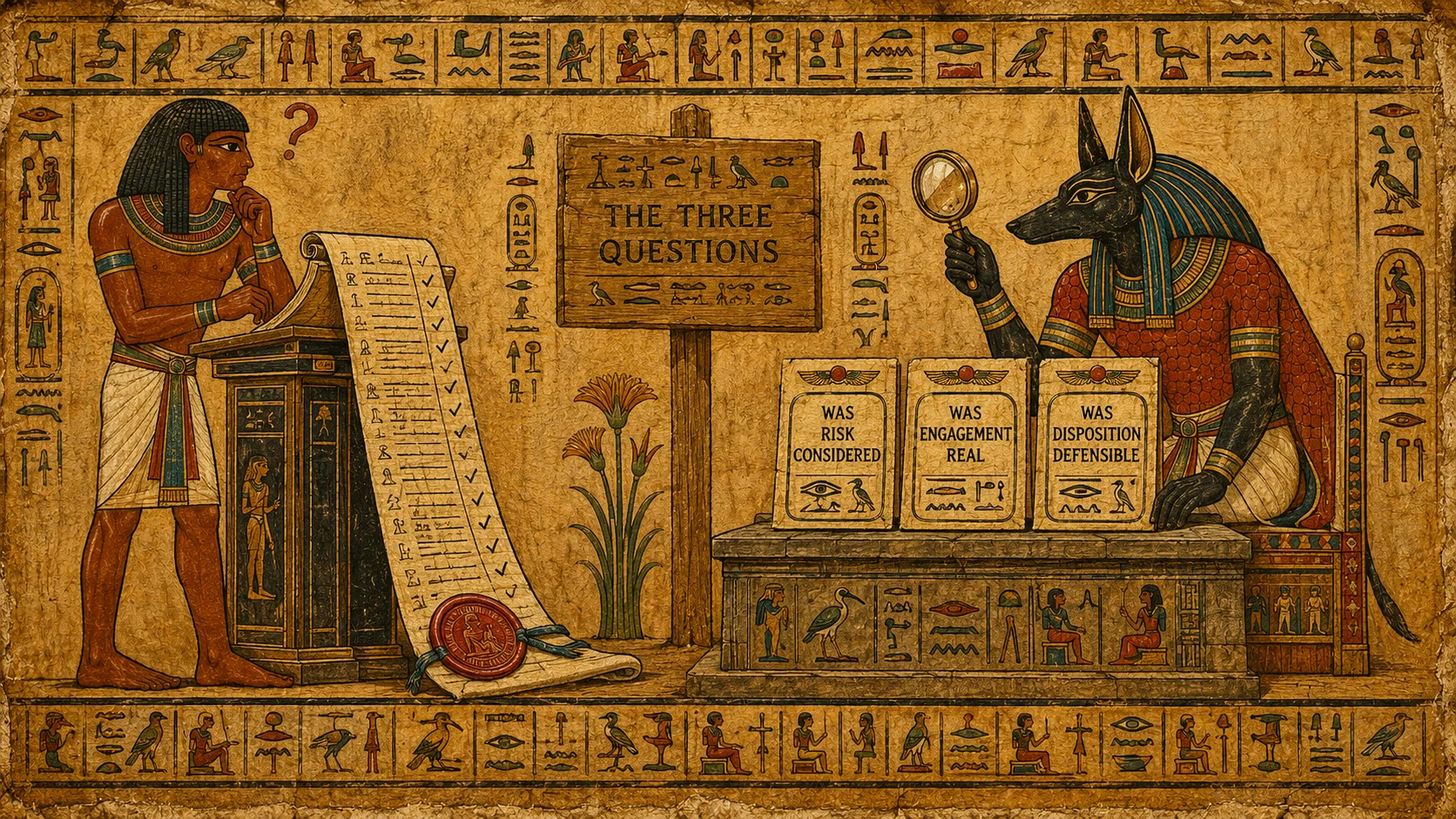

The three questions checkbox reviews cannot answer. Auditors ask them; the reviewer's scroll of uniform attestations cannot respond.

The three questions checkbox reviews cannot answer. Auditors ask them; the reviewer's scroll of uniform attestations cannot respond.

The three questions

Three questions dominate 2026 audit interviews about access reviews. Each is structural — the answer depends on how the review was architected, not on how well the reviewer completed it.

Question 1: Was risk actually considered?

Auditors expect that access reviews differentiate between high-risk entitlements and routine ones. Privileged admin access to financial systems, CDE-scoped grants, ePHI-access permissions, standing access to production databases — these are the entitlements a reasonable review pays careful attention to. Read-only access to a widely-shared knowledge base, entry-level role entitlements, low-sensitivity SaaS applications — these are entitlements a reasonable review can dispose of quickly.

A checkbox review treats every entitlement uniformly. The audit trail shows the same disposition (usually "approved") on the treasury operator's admin access to the general ledger as on the marketing intern's read-only access to a public wiki. Auditors ask: how could that be right? The high-risk grant should have received more scrutiny than the low-risk one; the uniform disposition suggests neither did.

Question 2: Was reviewer engagement real?

Auditors probe by asking reviewers to explain specific decisions from a completed review. "You approved user X's admin access to system Y — walk me through why." The auditor already knows the disposition from the record; they're testing whether the reviewer engaged with the decision or pattern-clicked through it.

Reviewers who examined each decision can articulate context: "Yes, I approved that — X is the deputy CFO, admin access is standard for the role, and I know she uses it monthly for closing procedures." Reviewers who pattern-clicked give blank looks: "Um, I don't remember specifically. I'm sure it was fine at the time."

A checkbox review provides no engagement evidence beyond the completion timestamp. If reviewers pattern-clicked, the record doesn't distinguish them from reviewers who engaged.

Question 3: Was disposition defensible?

For each entitlement, auditors expect a specific reason for the disposition beyond binary approve/revoke. "The user's role justifies this entitlement" is a minimum; "the user's role justifies this entitlement, the entitlement was used in the last 30 days, no SoD violation exists, and the assignment matches the documented role definition" is defensible. The context matters because it lets the auditor validate not just the disposition but the reasoning.

A checkbox review captures binary approve/revoke without underlying context. Auditors can see what was decided but not why the disposition was correct.

Comparison: checkbox vs risk-weighted review architecture

| Dimension | Checkbox review | Risk-weighted review |

|---|---|---|

| Entitlement presentation | Flat uniform list | Pre-stratified by risk (careful review / confirm bulk / recommend removal) |

| Reviewer attention | Uniform across all entitlements | Concentrated on high-risk decisions |

| Engagement evidence | Timestamp only | Time-on-decision, mouse-hover, periodic challenge, mandatory rationale |

| Disposition options | Binary approve/revoke | Approve with rationale / approve with mitigating control / revoke / defer to expert |

| Dormant entitlement handling | Same treatment as active | Recommended removal with reviewer override capability |

| SoD violation surfacing | Runs separately (or not at all) | Surfaced inline at the specific entitlements creating the violation |

| Behavioral usage data | Absent | Annotated per entitlement (last used, frequency, trend) |

| Cross-entitlement analysis | Absent | Anomaly surfacing (this user's grant is unusual for their role) |

| Audit trail | Completion timestamp + disposition | Full engagement + disposition rationale + supporting signals |

| Regime coverage from single review | Partial per regime | Full across SOX + PCI + HIPAA + SOC 2 simultaneously |

Every row differs. Cumulatively, the two architectures produce structurally different evidence trails when the auditor probes.

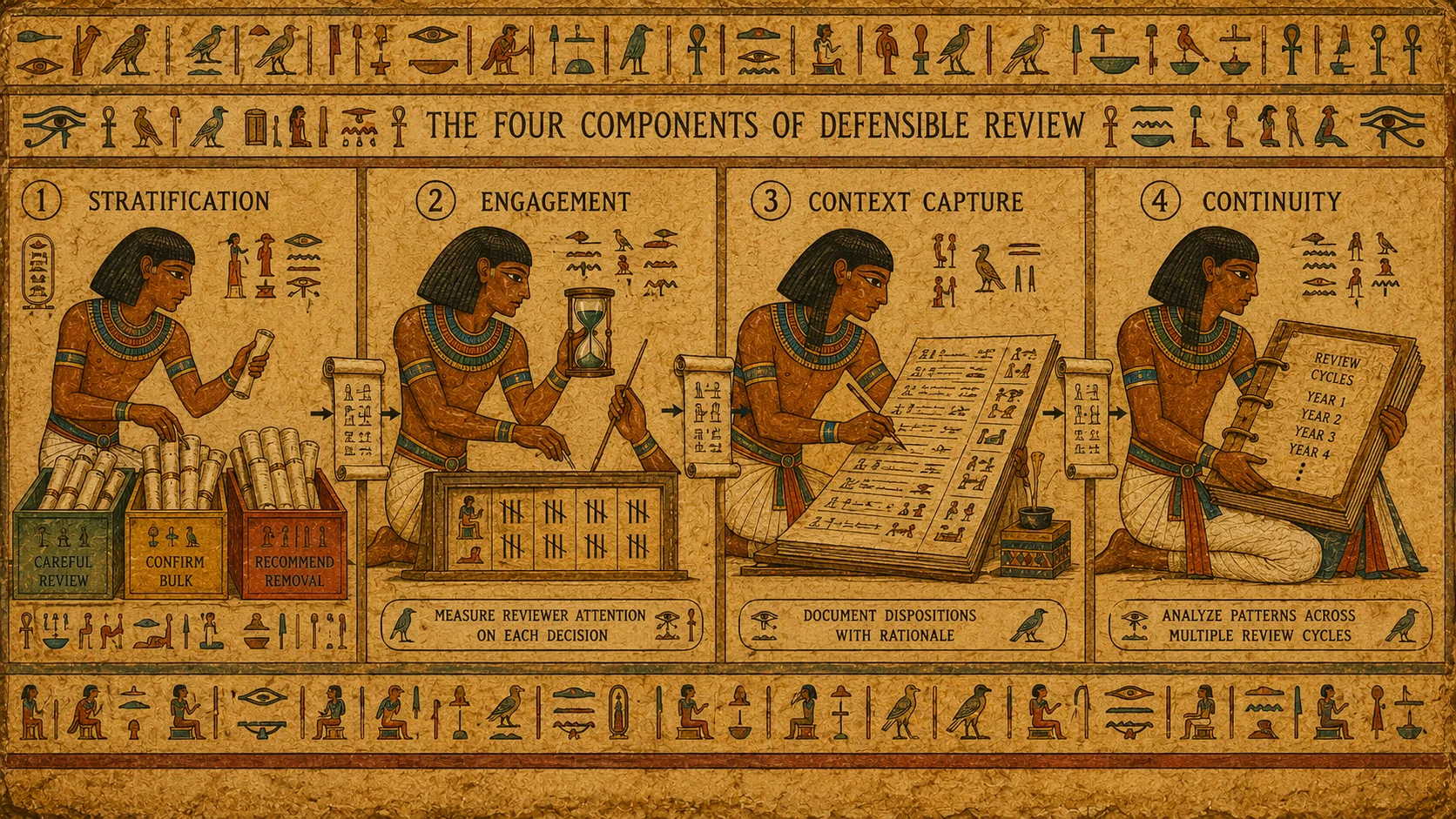

The four architectural components

The risk-weighted review architecture composes four operational components. Each addresses one of the three audit questions plus operational sustainability.

Component 1: Pre-stratification by risk. Before the reviewer sees the campaign, the IGA platform (or an ISPM tool composed with it) evaluates each entitlement against risk signals — sensitivity classification of the target system, sensitivity of the entitlement within the system, alignment between the user's current role and the entitlement's role basis, recent usage telemetry, cross-user comparison (is this entitlement unusual for the user's peer group), and any active risk flags on the user. Entitlements go into three or four buckets: careful review (the reviewer must engage), confirm bulk (the reviewer can approve in a batch decision), recommend removal (the AI recommends revocation unless the reviewer explicitly retains). The AI Access Certification piece covers the AI-augmented pattern in depth.

Component 2: Reviewer engagement instrumentation. Time-on-decision tracking (reviewers spending under a threshold get flagged for engagement audit), periodic challenge questions (a random subset of decisions asks the reviewer to briefly explain the disposition), mandatory rationale on high-risk buckets (the reviewer selects from a menu of rationales or free-texts an alternative). The instrumentation produces the engagement evidence auditor Question 2 asks for. Critically, the friction concentrates on pattern-clickers — engaged reviewers don't experience meaningful additional time cost.

Component 3: Disposition context capture. Each disposition records the reviewer's action plus the specific reason. Approve options include "role-appropriate and recently used," "role-appropriate but dormant, will monitor," "approved with mitigating control noted." Revoke options include "no current business justification," "SoD violation, remove," "dormant beyond retention window." The captured context lets auditors validate the disposition, not just observe it.

Component 4: Cross-review continuity. The IGA platform tracks review decisions over time so that disposition patterns become visible — a user's admin access approved four consecutive campaigns without change indicates stable entitlement; the same access with different reviewers each time approving without engagement indicates a pattern worth auditing. The cross-review view helps the compliance team identify weak review discipline before the auditor does.

The four components compose into an architecture where the three audit questions have structural answers. Question 1 (was risk considered) — yes, the pre-stratification is the direct evidence. Question 2 (was engagement real) — yes, the instrumentation traces are the evidence. Question 3 (was disposition defensible) — yes, the captured context is the evidence.

Four architectural components, one defensible review. Each component addresses one of the three auditor questions plus operational sustainability across cycles.

Four architectural components, one defensible review. Each component addresses one of the three auditor questions plus operational sustainability across cycles.

The compliance regime unification

The four regimes this series covers — SOX, PCI-DSS v4.0.1, HIPAA §164.312, SOC 2 CC6.x — differ in what they audit but expect the same underlying review discipline. A single risk-weighted review architecture covers all four simultaneously.

SOX §404 audits access to financial reporting systems. The risk-weighted review pre-stratifies financial-system entitlements by sensitivity, instruments reviewer engagement on high-risk grants (privileged access to ERP, treasury, general ledger), captures disposition context (role justification, usage evidence, SoD status), and produces cross-review continuity across quarterly cycles. Auditor questions get structural answers. The SOX Compliance piece covers the finding surface.

PCI-DSS v4.0.1 audits access to the CDE. Requirement 7.2.4 mandates access reviews at least every 6 months for user accounts and 7.2.5 for application accounts. The same risk-weighted architecture handles both — CDE-scoped entitlements go into the careful-review bucket, service accounts follow the same discipline as human accounts (v4.0.1 tightened this), and the 6-month cadence is operationally sustainable because the review isn't a full manual sweep. The PCI-DSS v4.0.1 piece covers the finding surface.

HIPAA §164.312 audits ePHI access. The Security Rule doesn't specify review cadence directly, but §164.308(a)(4)(ii)(C) administrative safeguards do require periodic evaluation and access reviews are the operational instantiation. The risk-weighted architecture handles ePHI-access entitlements (careful review), delegate-access grants (careful review with delegator confirmation), and shared-workstation authentication (usually out of scope for entitlement review but in scope for the audit-controls layer). The HIPAA §164.312 piece covers the finding surface.

SOC 2 CC6.1-CC6.3 audits logical access controls for the service scope. The Trust Services Criteria expect access to be granted based on documented need, restricted per policy, and reviewed periodically. The risk-weighted architecture handles all three — the pre-stratification implements the risk consideration, the instrumentation implements the review discipline, the disposition context implements the periodic review evidence.

Same architecture, four regime-specific finding surfaces defended simultaneously. The operational efficiency alone makes the risk-weighted pattern worth the investment; the audit defensibility is the compounding benefit.

Reviewer engagement without productivity theater

The instinct to over-instrument reviewer engagement produces its own compliance failure — reviewers rebel against the friction, reviews get delegated or ignored, and the engagement metrics look good but the review outcomes are worse. Three principles for engagement instrumentation that works:

Principle 1: Friction concentrates on pattern-clickers. Time-on-decision tracking, sampling challenge questions, and mandatory context on high-risk buckets all impose minimal load on engaged reviewers and meaningful load on disengaged ones. That's the intended outcome — the reviewer who's actually looking at each decision spends a few extra seconds selecting a rationale menu item; the reviewer who's pattern-clicking gets interrupted by challenges that break the pattern.

Principle 2: Sampling, not surveillance. Challenge questions on every decision is surveillance and reviewers hate it. Challenge questions on 5-10% of decisions, chosen randomly, is sampling — the reviewer doesn't know when a challenge is coming, so they engage on every decision, but the actual challenge frequency is manageable. The sampling produces enough engagement evidence for the audit without imposing continuous friction.

Principle 3: High-risk buckets get more discipline; routine buckets get less. The confirm-bulk bucket doesn't need engagement instrumentation — the whole point of stratifying it as bulk is that the reviewer can dispose of it efficiently. The careful-review bucket needs the full discipline. The proportionate approach preserves reviewer efficiency where the risk profile allows it and concentrates discipline where the risk profile demands it.

The three principles compose. Instrumentation is real but proportionate. Engaged reviewers barely notice; pattern-clickers get interrupted; the evidence trail supports the audit.

The Avatier compliance posture matters for customer audit programs

Customer audit teams evaluating whether their IGA vendor supports defensible access reviews increasingly probe the vendor's own review discipline. If the vendor's platform doesn't support risk-weighted reviews, or if the vendor's own compliance program uses checkbox reviews, that's a signal about how the platform will support the customer.

Avatier maintains a comprehensive compliance posture published at the Avatier Trust Center:

- SOC 2 Type II with zero exceptions — including the logical access control criteria (CC6.1-CC6.3) that audit access reviews

- ISO/IEC 27001:2022 — including Annex A.5.15-5.18 which cover access management and review discipline

- PCI DSS v4.0.1 — including the Requirement 7.2.4 and 7.2.5 access review cadence

- CSA STAR Level 1

- NIST 800-53 Rev. 5 aligned — including AC-2 (account management) and AC-6 (least privilege) control families

- CISA Secure-by-Design Pledge signatory

The third-party security-grades view (SecurityScorecard) is at trust.avatier.com/?itemName=security_grades — customer audit teams can validate Avatier's independent security posture without procurement questionnaires.

Avatier's platform supports the risk-weighted review architecture this piece describes; Avatier's own compliance program uses the same discipline internally; the outcomes are published in the Trust Center. Customer audit programs benefit from the alignment.

The 2026 reference path

Move from checkbox reviews to risk-weighted reviews. The three audit questions — was risk considered, was engagement real, was disposition defensible — have structural answers only when the review architecture is designed around them. Pre-stratification by risk. Engagement instrumentation that concentrates friction on pattern-clickers. Disposition context capture that supports auditor validation. Cross-review continuity that surfaces disposition patterns.

Deploy the AI-augmented certification pattern as the platform component. The AI Access Certification piece covers the operational architecture; the Revolutionize Access Certification post on avatier.com covers the operational pattern.

Compose with the broader compliance stack. The risk-weighted review is one layer; HRIS-driven lifecycle prevents entitlement drift between reviews (HRIS-Driven Lifecycle piece), ISPM catches drift between review cycles (ISPM piece), ITDR detects active abuse of granted entitlements (ITDR piece), and the Maturity Model piece locates where a program sits.

Use the same review architecture across all compliance regimes. SOX, PCI-DSS v4.0.1, HIPAA §164.312, and SOC 2 CC6.x all reward the same underlying discipline. One architecture defends four regime surfaces simultaneously.

Point auditors at the Avatier Trust Center with the SecurityScorecard grade view for Avatier's own compliance posture — vendor-management artifact gathering shortens from weeks to minutes.

Access reviews are one of the most consistently under-performing compliance activities in modern IT. The three audit questions expose why checkbox reviews fail. The risk-weighted architecture addresses each question structurally. The compliance regimes reward the same underlying discipline. Build the review architecture deliberately — the audit cycles of 2027, 2028, and 2029 will reward the choice.

ABOUT THE AUTHOR

More from Compliance & Audit

SOX Compliance for Identity Teams 2026: What Auditors Actually Want to See

Sarbanes-Oxley Section 404 places IT general controls (ITGC) over financial systems squarely in the IAM team's lap — even though SOX itself doesn't mention identity once. The 2026 enterprise reference on the five SOX ITGC domains that depend on identity controls, the auditor expectations that shifted in the post-2025 audit cycle, and the architecture that produces clean SOX walkthroughs.

HIPAA Access Audits for Healthcare Identity Teams 2026

HIPAA Security Rule § 164.312 places identity controls at the center of every covered entity's access-audit risk. OCR enforcement actions have intensified through 2024-25, and the 2026 audit profile is substantively harder than the prior decade. The enterprise reference on the five Technical Safeguards that depend on identity controls, the post-2024 OCR enforcement pattern, and the architecture that produces defensible HIPAA access-audit posture for healthcare IT.

The Access Review Your Auditor Actually Wants 2026

Most enterprise access reviews are checkbox exercises — manager attests, audit log records, cycle closes. The auditor walks away with a binder of attestation evidence and the program reports clean. The 2026 auditor profile asks harder questions: did the reviewer actually engage, does the catalog match target-system reality, and what changed as a result. The enterprise reference on the three questions auditors actually ask now and the five review patterns that pass the test.